")

Banking and Operational Readiness for ADGM Bank Account and DIFC Bank Account Setup in UAE

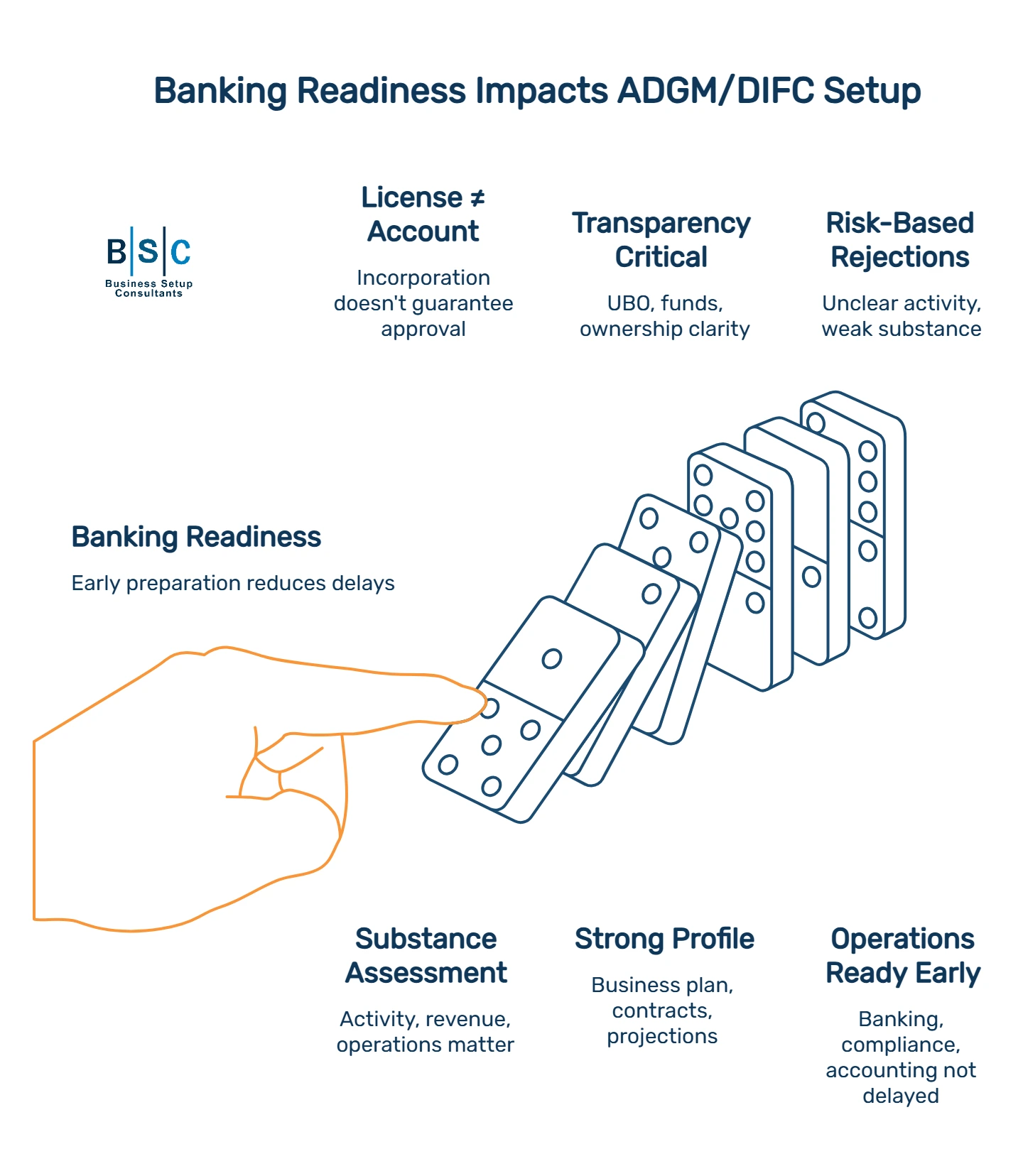

Acquiring a license in ADGM or DIFC appears to be a milestone but the operational readiness starts when compliance, banking and business activities align successfully.

Most business founders think that company incorporation will guarantee immediate banking accessibility.

However, in reality, securing one ADGM bank account or DIFC bank account demands commercial substance demonstration by the business. It also requires operational preparedness and regulatory compliance to assess risk profiles.

This turns post-incorporation readiness as significant for business priority.

Banking readiness

Business credibility is often evaluated by banks, not merely corporate existence.

Here are some core banking readiness factors:

| Assessment area | Bank focus |

| Business activity | Commercial legitimacy. |

| Ownership structure | UBO transparency. |

| Funding source | Financial traceability. |

| Business model | Revenue generation. |

| Geographic exposure | Risk assessment. |

| Compliance profile | Regulatory alignment. |

Readiness checklist

- Verified shareholder information.

- Defined business activities.

- Clear source of wealth documentation.

- Commercial contracts or pipeline evidence.

- Proper corporate governance records.

- Operational website and digital presence.

Onboarding expectations

Bank onboarding stands as a compliance exercise just as it stands as a banking process.

Financial institutions typically demand:

- Customer and supplier information.

- Shareholder identification documents.

- Detailed business plan.

- Transaction volume projection.

- Regulatory compliance declaration.

- Operational presence and proof.

Key objective: Banks demand assurance that the company presents a sustainable and transparent business profile.

Rejection patterns

Often account rejections developed from risk concern instead of documentation shortage.

Common reasons involve the following:

- High risk jurisdiction.

- Weak economic substance.

- Financial information inconsistency.

- Complex ownership structure.

- Compliance response inadequacy.

- Unclear business activities.

Risk perspective: A licensed entity may suffer banking challenges if it fails in demonstrating operational credibility.

Operational gaps after licensing

Licensing establishes legal existence while operations develop commercial functionality.

Common gaps include:

- Banking arrangement delay.

- Accounting system absence.

- Missing compliance procedure.

- Shortage of customer onboarding process.

- Poor governance framework.

Priority areas

- Corporate compliance.

- Financial control.

- VAT readiness.

- Regulatory reporting.

- Banking relationships

Conclusion

A successful ADGM or DIFC setup is measurable not by incorporation but through operational activation. Securing one DIFC Bank account or ADGM bank account demands regulatory transparency, operational substance and strategic preparation.

Businesses aligning licensing, governance, compliance and banking through the outset are more suitably positioned in terms of seamless market entry and sustainable growth.

Get our PRO support to achieve banking and operational assistance regarding ADGM & DIFC company setup.

Frequently Asked Questions (FAQs)

Does ADGM or DIFC licensing guarantee bank account approval?

No, ADGM and DIFC licensing does not guarantee rather banks conduct independent compliance and risk assessments.

Why do banks demand detailed business information?

Banks request detailed business information in order to satisfy KYC, AML and regulatory obligations.

What is the most common reason for bank account rejection in the UAE?

Insufficient business substance or unclear transaction activity is the main cause of bank account rejection in the UAE.

Is a business plan necessary for ADGM or DIFC bank account approval?

Many banks including ADGM or DIFC demand a business plan for onboarding reviews in the UAE.

When should banking preparation begin for business setup in the UAE?

Banking preparation ideally needs to start before company incorporation in order to minimise onboarding delays.